Is Home Loan Insurance Mandatory in 2026? Truth Exposed

Avoid bank upsells with the official RBI rules on home loan insurance in 2026. Save lakhs using term insurance instead of bundled plans.

"No, home loan insurance is not mandatory. The Reserve Bank of India (RBI) and IRDAI clarify that lenders cannot force you to buy insurance to approve a loan. It is entirely voluntary. You can choose to skip it, buy it from an independent provider, or substitute it with a standard term insurance policy."

Is Home Loan Insurance Mandatory? The Truth Banks Do Not Want You To Know

Imagine signing your dream home papers, only to find an extra Rs 2.5 lakh added to your total loan amount. Your loan agent insists you cannot get the loan approved without this mortgage protection plan. Is this true?

Let us look at the facts.

No. The Reserve Bank of India (RBI) and the Insurance Regulatory and Development Authority of India (IRDAI) do not make home loan insurance mandatory. It is a voluntary product. Banks cannot legally force you to buy it to approve your loan.

Why Lenders Push These Plans

Many Indian home buyers face intense pressure to buy a Mortgage Triparty Plan or Single Premium Term Insurance. Loan officers often bundle this premium directly into your main home loan.

If you borrow Rs 50 lakh, the bank might add a Rs 2 lakh insurance premium, raising your actual loan to Rs 52 lakh. Now, you pay interest on Rs 52 lakh.

Here is why this hurts your pocket. If you take a loan from State Bank of India at current interest rates of 7.25% to 8.40%, that extra Rs 2 lakh premium costs you thousands in interest over 20 years.

The official RBI website (rbi.org.in) states that tying a loan approval to the purchase of insurance is an unfair practice. You have the complete freedom to choose your insurance provider or skip it entirely.

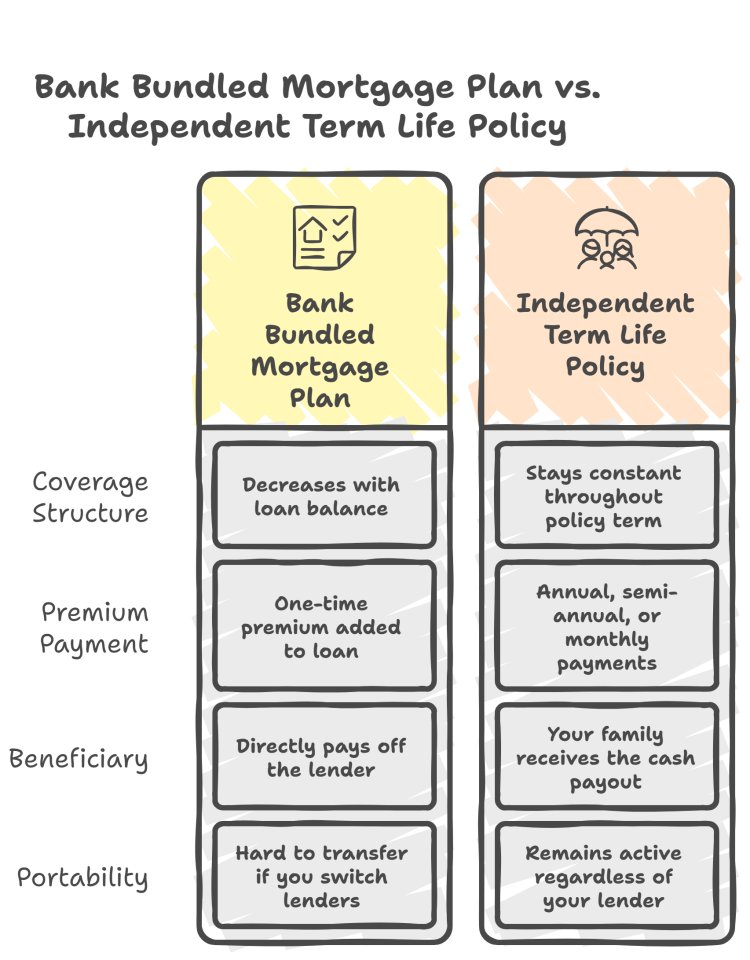

Comparing Bank Policies with Term Insurance

Let us evaluate the differences between bank-bundled plans and buying your own policy.

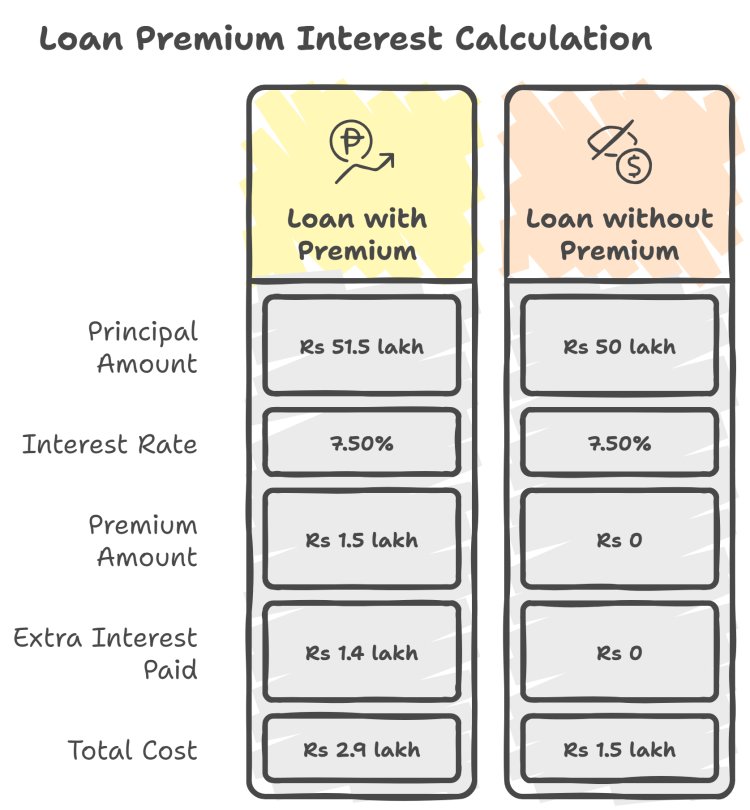

The Cost of Bundled Premiums

When a lender bundles your premium into your loan, you pay compound interest on that premium.

Let us calculate this.

Imagine you take a Rs 50 lakh loan at HDFC Bank's active rate of 7.50%. If the bank adds a Rs 1.5 lakh insurance premium to the loan, your new loan principal becomes Rs 51.5 lakh.

Over a 20-year tenure, you do not just pay Rs 1.5 lakh. You pay over Rs 1.4 lakh extra in interest. That is a total cost of Rs 2.9 lakh for a policy that only covers your declining loan balance.

How Amit Saved Rs 1.8 Lakh

Amit, a software engineer in Pune, applied for a Rs 60 lakh loan. The lender insisted on a Rs 1.85 lakh single-premium mortgage protection plan.

Instead of accepting, Amit checked the RBI rules. He purchased a pure term life insurance policy online for an annual premium of Rs 12,000. He presented this policy to the bank, listing them as the nominee.

The bank accepted it. Amit saved the upfront Rs 1.85 lakh and avoided paying interest on it for two decades.

Your Plan at the Bank Counter

Here is your step-by-step strategy to handle this:

First, ask for a written rejection if the bank refuses your loan without insurance. Lenders will back down quickly. They cannot put this demand in writing because it violates RBI rules.

Second, offer your existing term insurance policy as security.

Third, compare rates across lenders. If one lender insists on bundling, check LIC Housing Finance starting at 7.25% or Bank of Baroda starting at 7.15%.

You can navigate these banking steps easily. QuickHome Loan helps you compare real, unbundled rates across major Indian banks so you never pay for unwanted add-ons.

Key Points & Takeaways:

- Home loan insurance is legally voluntary according to RBI and IRDAI guidelines.

- Bundling insurance premiums into your loan increases your principal and results in heavy interest costs.

- An independent term insurance policy is cheaper, keeps coverage constant, and remains active if you switch lenders.

- You can decline bank-bundled insurance by offering an existing term policy or demanding a written rejection letter.

Frequently Asked Questions (FAQ)

Q: Can a bank reject my home loan if I refuse to buy insurance?

A: No, a bank cannot legally reject your loan application solely because you refuse their bundled insurance plan. Doing so violates RBI fair practice codes.

Q: Is a normal term insurance policy sufficient for a home loan?

A: Yes, a standard term life insurance policy is a great substitute. You can assign the policy to the bank as security, which is often much cheaper than a bank-bundled mortgage protection plan.

Q: Do I get a refund on home loan insurance if I prepay my loan?

A: If you pay off your loan early, you can request a pro-rata refund on your single-premium insurance policy, though banks often make this process tedious.