Emergency Fund vs Home Loan Prepayment: Where to Put Your Money First

Deciding between saving an emergency fund or prepaying your home loan? Learn the tax-saving math and risk rules to maximize your surplus cash.

"Build your emergency fund covering six months of expenses before prepaying your home loan. Prepaying saves you a guaranteed, tax-free interest rate of 7.25% to 8.55%, but illiquid home equity cannot pay for sudden emergencies. Secure your cash safety net first, then prepay your principal."

Emergency Fund vs Home Loan Prepayment: Where to Put Your Money First

Imagine prepaying Rs 5 Lakh of your home loan, only to face a medical emergency next month. You cannot pull that prepaid money back from your bank. This classic trap leaves Indian home buyers asset-rich but cash-poor. Let's look at how to balance your safety net and your debt.

What is the quick rule for Emergency Fund vs Home Loan Prepayment?

Put your money into an emergency fund before making a single home loan prepayment. Financial security requires liquid cash. Only when you have six months of living expenses, including your loan EMIs, should you route your surplus toward prepayment.

Let's compare the financial math

With the RBI repo rate holding steady at 5.25%, which you can verify on the official RBI website (rbi.org.in), major banks like SBI offer home loan rates between 7.25% and 8.40%. HDFC and ICICI sit slightly higher at 7.50% to 8.55%.

When you prepay, you earn a guaranteed return equal to your loan interest rate. Here is how that compares to other options:

| Financial Action | Average Annual Return | Liquidity Level | Tax Implications |

|---|---|---|---|

| Home Loan Prepayment | 7.25% to 8.55% | Zero (Very Low) | Reduces Section 24b deduction room |

| Debt Mutual Funds | 6.00% to 7.00% | High (1-2 days) | Taxed at your income slab rate |

| Equity Mutual Funds | 11.00% to 13.00% | Moderate (3 days) | 12.5% LTCG tax above limit |

Let's break down the return rate. Prepaying a loan at 7.25% is mathematically identical to earning a tax-free 7.25% return.

Tax write-offs and the real cost of debt

Your home loan interest offers deductions under Section 24b of the Income Tax Act up to Rs 2 Lakh per year in the old tax regime. If you fall in the 30% tax bracket, a 7.25% interest rate actually costs you only around 5.07% after tax benefits.

Here is why this matters. If your post-tax loan cost is 5.07%, and equity funds yield 11.00%, keeping the loan and investing the surplus might build more wealth. But if you choose the new tax regime, you lose the Section 24b deductions for self-occupied properties. Without this write-off, prepaying yields the full 7.25% to 8.55% risk-free return, making it far more attractive.

The safety net story: Why liquidity wins

Amit had a home loan of Rs 50 Lakh at SBI with an interest rate of 7.25%. He received a bonus of Rs 3 Lakh. He wanted to prepay his loan to reduce his EMI. Instead of prepaying the whole amount, he kept Rs 2 Lakh in a high-yield liquid account and prepaid only Rs 1 Lakh.

Three months later, his company faced a sudden restructuring. Because he kept liquid cash, he easily paid his monthly EMI of Rs 40,000 without defaulting. Had he prepaid the entire Rs 3 Lakh, his bank account would have been empty, leading to credit score damage and penalty fees.

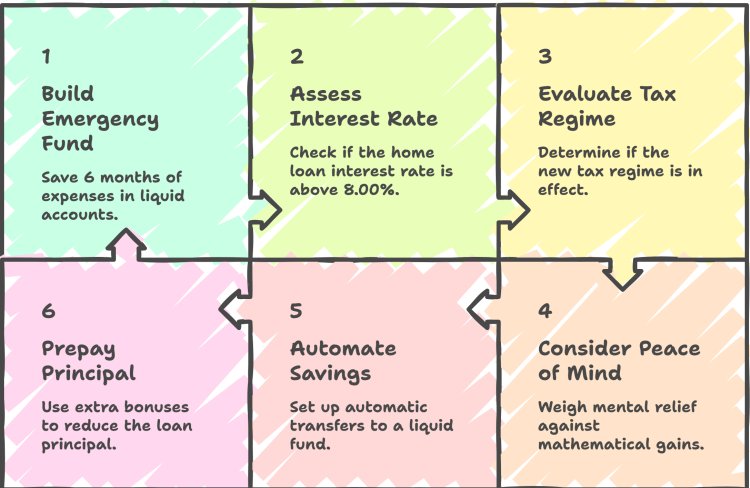

Your immediate action plan

Use these direct questions to decide your next step:

- Do you have 6 months of expenses, including home loan EMIs, saved in liquid accounts? If no, build your emergency fund.

- Is your home loan interest rate above 8.00%? If yes, prepayment becomes a smart priority once your emergency fund is secure.

- Are you under the new tax regime? If yes, you get no Section 24b tax benefit, making prepayment smarter.

- Do you value peace of mind over raw mathematical gains? If yes, prepaying your debt relieves mental pressure.

Next steps. Start by automating a small transfer to a separate liquid mutual fund or savings account. Once that matches six EMIs and living costs, direct all extra bonuses to prepaying your home loan principal.

QuickHome Loan is here to help you navigate these choices with transparent calculators and expert guidance, helping you build real security.

Key Points & Takeaways:

- Always establish a liquid six-month emergency fund before prepaying your home loan.

- Prepaying a home loan offers a risk-free, guaranteed return equal to your interest rate (7.25% - 8.55%).

- Under the new tax regime, the lack of Section 24b deductions makes prepayment more financially attractive.

- Home loan prepayment is completely illiquid, meaning you cannot access that cash in an emergency.

Frequently Asked Questions (FAQ)

Q: Can I withdraw money once I prepay a home loan?

A: No. Once you prepay your home loan, the bank applies those funds directly to reduce your outstanding principal. You cannot easily withdraw this cash back for emergencies.

Q: Does prepaying a home loan reduce my tax benefits?

A: Yes. If you prepay your home loan under the old tax regime, your outstanding principal and annual interest payments drop. This can reduce the deduction you claim under Section 24b.

Q: How many EMIs should be in my emergency fund?

A: Your emergency fund should cover at least six months of total living expenses, which must include your monthly home loan EMIs.