Where to Park Your Monthly Surplus: Savings vs FD vs Liquid Funds

Discover where to park your monthly surplus. Compare savings accounts, FDs, and liquid funds to grow your cash safely for a home down payment.

"Park your monthly surplus based on when you need it. Keep immediate bill money in a savings account. Route your emergency fund and short-term savings into Fixed Deposits (FDs) for guaranteed returns, or liquid mutual funds for flexible, penalty-free growth that tracks the active 5.25% RBI repo rate."

Savings Account vs FD vs Liquid Fund: Where to Park Your Monthly Surplus

Are you leaving your hard-earned money to rot in a basic savings account? Many Indian households let their monthly surplus sit idle, earning a measly 3% interest. That is a silent tax on your wealth. If you are saving for a home down payment or building an emergency fund, you need your money to work.

Let us explore the three main options for your cash: savings accounts, fixed deposits, and liquid mutual funds.

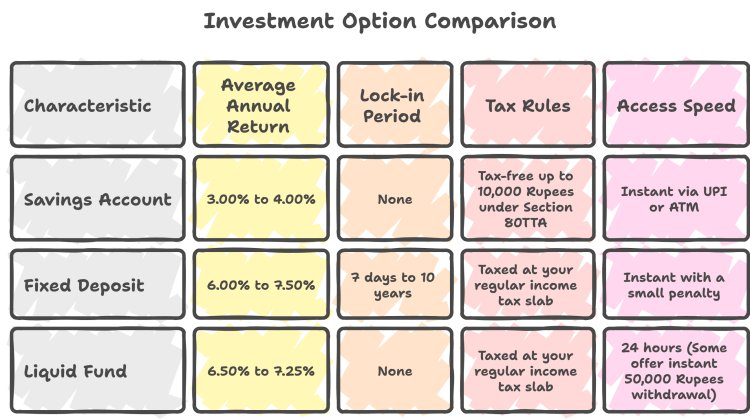

The Core Differences: Savings vs FD vs Liquid Funds

Here is how the three choices compare right now:

Let us break down each option to find the best fit for your surplus.

Savings Accounts: Best for Ultra-Short-Term Liquidity

Savings accounts offer absolute safety and speed. You can withdraw your money at midnight using UPI or an ATM card.

However, safety comes at a price. Standard banks offer low rates, often failing to beat inflation. Keep only your immediate monthly household expenses here.

Fixed Deposits: Best for Guaranteed Short-Term Goals

Fixed deposits offer a guaranteed return. When you book an FD, the interest rate stays the same throughout the tenure, even if the market rates drop.

Most major banks, including State Bank of India, HDFC Bank, and ICICI Bank, offer solid FD rates today. If you plan to buy a home in the next twelve months, booking an FD protects your capital.

The catch? If you break the FD early, banks charge a premature withdrawal penalty of 0.5% to 1.0%.

Liquid Funds: Best for Flexible Growth

Liquid funds are mutual funds that invest in short-term government securities and certificates of deposit.

They do not offer guaranteed returns like FDs, but they usually track the repo rate closely. They offer excellent flexibility. You can withdraw your money without any penalty after seven days.

For tax-paying individuals in the highest income bracket, liquid funds do not offer long-term capital gains benefits anymore. They are taxed at your slab rate, matching FDs.

How Amit Lost 50,000 Rupees by Playing It Too Safe

Let us look at a real-life scenario.

Amit wanted to accumulate 10 Lakh Rupees for a down payment on a flat. He started saving 50,000 Rupees every month. Fearful of the market, he kept all his money in a standard savings account earning 3% interest.

Over two years, his savings grew, but his interest earnings remained low.

If Amit had routed his monthly surplus into a short-term FD or a liquid fund earning an average of 7% interest, he would have earned an extra 50,000 Rupees. That is equivalent to almost two monthly EMIs on a future home loan of 35 Lakh Rupees.

Your Three-Step Surplus Routing Plan

How should you manage your cash flow? Here is a simple plan:

First, keep one month of living expenses in your regular savings account. This covers your daily UPI payments and bills.

Second, build an emergency fund worth six months of expenses. Split this fifty-fifty between a fixed deposit and a liquid fund.

Third, park any extra money meant for your upcoming home down payment in a liquid fund. This keeps your capital safe while earning more than a basic savings account.

At QuickHome Loan, we help you prepare for your home buying plans by showing you how to manage your cash flow. A healthy savings habit makes getting a home loan approval much easier.

Key Points & Takeaways:

- Savings accounts are best for immediate expenses but fail to beat inflation.

- Fixed deposits offer guaranteed returns ideal for goals within one year.

- Liquid funds offer flexible, penalty-free growth for short-term surpluses.

- The 5.25% RBI repo rate directly influences the returns of all three options.

- A smart routing plan secures your emergency fund while growing your down payment.

Frequently Asked Questions (FAQ)

Q: Is a liquid fund safer than a fixed deposit?

A: Fixed deposits are safer because they offer guaranteed returns and are insured up to 5 Lakh Rupees per bank. Liquid funds carry minimal market risk but do not offer guaranteed returns.

Q: Can I withdraw money instantly from a liquid fund?

A: Most liquid funds credit your bank account within one business day. Some funds offer instant redemption up to 50,000 Rupees per day.

Q: How are liquid funds taxed in India?

A: Liquid fund gains are added to your taxable income and taxed according to your regular income tax slab rate, similar to fixed deposit interest.