How to Manage Multiple Loans Without Breaking Your Monthly Budget

Learn how to manage multiple loans including home, car, and personal loans. Master your monthly EMIs with practical cash flow tips based on current RBI rates.

"To manage multiple loans successfully, keep your total monthly EMIs below 50% of your net take-home pay. Prioritize paying off high-interest unsecured debts like personal loans first while maintaining regular payments on your home and car loans. Consider refinancing or using home loan top-ups to consolidate expensive debts."

How to Manage Multiple Loans Without Ruining Your Monthly Budget

Imagine looking at your bank statement and seeing three different EMIs exit your account in the first week of the month. One payment goes to your home, another to your hatchback, and a third to that personal loan you took for an emergency.

If you struggle to manage multiple loans every month, you are not alone. Millions of Indian borrowers face this exact cash flow squeeze. Let us look at how you can organize your finances and protect your savings.

The Real Cost of Juggling Multiple EMIs

Let us look at a typical Indian household. Amit earns 1.5 Lakh Rupees a month. He pays 50,000 Rupees for his home loan, 15,000 Rupees for his car loan, and 10,000 Rupees for a personal loan. That is 75,000 Rupees gone before he buys groceries. He has hit the 50 percent debt-to-income limit, leaving his household budget highly vulnerable to emergencies.

To keep your finances safe, you must track where your money goes. Different loans carry vastly different interest rates.

| Lender and Loan Type | Active Interest Rate Range | Impact on Your Monthly Budget |

|---|---|---|

| State Bank of India Home Loan | 7.25% to 8.40% | Long term, lowest rate, builds a real asset |

| HDFC and ICICI Bank Home Loans | 7.50% to 8.55% | Stable long term rates, tied to market benchmarks |

| Standard Car Loans | 8.50% to 10.50% | Medium term, depreciating asset value |

| Unsecured Personal Loans | 11.00% to 15.00% | Short term, very high interest cost |

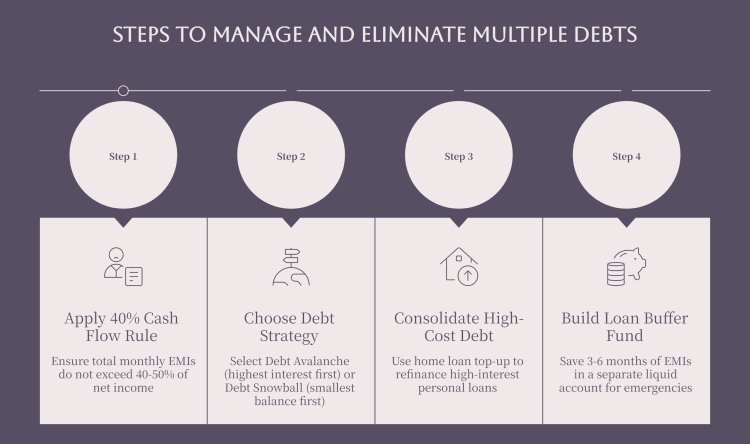

Step 1: Apply the 40 Percent Cash Flow Rule

Your first line of defense is your debt-to-income ratio. As a healthy rule of thumb, your total monthly EMIs should not exceed 40 to 50 percent of your net monthly income.

If your EMIs exceed this threshold, you need to act quickly. Start by reviewing your monthly bank statements. Look for non-necessary expenses that you can pause temporarily to free up cash for loan prepayments.

Step 2: Choose Your Debt Elimination Strategy

When you have multiple active debts, you can use two well-known strategies to clear them.

First, the Debt Avalanche. With this path, you direct every extra Rupee toward the loan with the highest interest rate while paying the minimum balance on others. In Amit's case, he would target his 14 percent personal loan first. This strategy saves you the most money in interest over time.

Second, the Debt Snowball. Here, you focus on paying off the smallest loan balance first, regardless of the interest rate. Once you clear that small loan, you get a psychological boost and move the freed cash to the next loan. This is perfect if you need quick wins to stay motivated.

Step 3: Consolidate High Cost Debt Using Home Loan Top-Ups

If your personal loan is choking your monthly cash flow, a home loan top-up can save you. Banks like SBI and Bank of Baroda offer top-up loans at interest rates close to their standard home loan rates, which range from 7.15 percent to 8.40 percent.

Using a top-up loan to pay off a 14 percent personal loan can slash your interest payments by nearly half. Be careful, though. Doing this extends the life of your debt, so try to make prepayments whenever you receive a bonus or annual raise.

Step 4: Build a Dedicated Loan Buffer Fund

When you manage multiple loans, a sudden job transition or medical emergency can cause a missed payment. A single missed EMI can damage your CIBIL score instantly.

Set aside at least three to six months worth of total EMIs in a separate liquid savings account. Do not touch this money for regular expenses. Use it only if your primary income source is temporarily disrupted.

Next Steps for Your Financial Peace of Mind

Managing your monthly payments does not have to be a source of constant stress. By categorizing your loans by interest rate and systematically targeting the most expensive ones, you can reclaim control of your bank account.

If you want to explore refinancing your home loan or accessing a low-cost top-up to clear your personal debts, our team at QuickHome Loan can guide you through the process step by step.

Key Points & Takeaways:

- Keep your total monthly EMIs below 40 to 50 percent of your net income to prevent cash flow strain.

- Prioritize paying off unsecured, high-interest personal loans before focusing on home loans.

- Use the debt avalanche method to target loans with the highest interest rates first to save maximum money.

- Keep a dedicated emergency buffer of three to six months worth of EMIs to protect your CIBIL score from unexpected income drops.

Frequently Asked Questions (FAQ)

Q: Which loan should I pay off first if I have a home, car, and personal loan?

A: You should generally pay off your personal loan first. Personal loans carry the highest interest rates (often 11% to 15%) and offer no tax benefits, unlike home loans.

Q: Does paying off my car loan early help my home loan eligibility?

A: Yes. Eliminating your car loan EMI lowers your debt-to-income ratio. This makes you much more eligible for a higher home loan amount with better terms.

Q: Can I use a home loan top-up to close a personal loan?

A: Yes, you can use a home loan top-up to close high-cost debts. Top-up interest rates are much lower than personal loan rates, which helps lower your overall monthly interest burden.