NPS vs EPF vs PPF: Best Retirement Plan in India

Compare NPS, EPF, and PPF to build your retirement corpus with active interest rates and tax benefits

"For maximum safety and tax-free returns, choose PPF. If you are salaried, prioritize EPF for guaranteed employer matching. To beat long-term inflation with equity exposure, allocate funds to NPS. A balanced mix of all three offers the best security and growth for your retirement corpus."

The Retirement Trap You Must Avoid

Let us break down a common myth. Most people believe that sticking to a single savings scheme will secure your post-retirement life. It will not. Inflation quietly chips away at your purchasing power while you sleep.

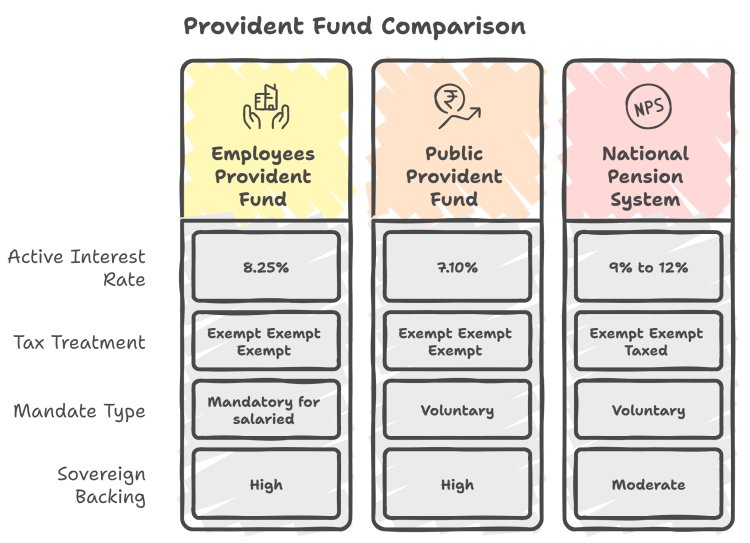

Building a secure retirement corpus requires a smart mix of safety, tax savings, and market growth. In India, three heavyweights dominate this space: the National Pension System, the Employees Provident Fund, and the Public Provident Fund.

Here is how they stack up against each other under current financial guidelines.

Understanding the Three Heavyweights

Employees Provident Fund remains the bedrock for salaried employees. Your employer matches your 12% basic salary contribution, giving you an automatic head start. The current interest rate of 8.25% makes it one of the highest-yielding fixed-income instruments in the country.

Next, we have the Public Provident Fund. It is the ultimate tax-free safe haven. You can deposit up to 1.5 Lakh Rupees per financial year. Every rupee of interest you earn and the final maturity amount remain completely tax-free. Since the government backs it, you face zero market risk.

National Pension System is your growth engine. Unlike the other two, it invests a portion of your money in equities. If you want to beat inflation over twenty or thirty years, you need equity exposure. It offers up to 75% equity allocation, helping you build a larger wealth pool.

The Home Loan and Retirement Connection

How does this tie into your larger financial life?

Let us look at a realistic scenario. Consider Rohan, a 30-year-old IT professional earning 1.5 Lakh Rupees a month net. He wanted to buy a home and secure his retirement.

Rohan made a common mistake. He wanted to dump his entire monthly savings into a heavy home loan monthly installment. I advised him against this. A healthy financial plan limits your home loan monthly installment to 35% of your take-home pay. For Rohan, that meant keeping his payment under 52,500 Rupees.

By keeping his home loan installment capped, Rohan freed up money to split between his provident fund and pension accounts. This balance protected his retirement while allowing him to buy his dream home using a competitive home loan.

When you plan your home purchase, you must look at active market rates. Currently, major banks offer competitive terms. For reference, State Bank of India home loan rates sit between 7.25% and 8.40%, while private lenders like HDFC and ICICI Bank offer rates between 7.50% and 8.55%. These home loan options work best when your retirement funds remain untouched.

Your Step-by-Step Wealth Roadmap

Here is your action plan to balance retirement and home ownership:

- Secure your employers full match on your provident fund.

- Maximize your Public Provident Fund up to 1.5 Lakh Rupees for tax-free safety.

- Allocate 50,000 Rupees to the National Pension System for extra tax deductions.

- Set aside a six-month emergency fund before applying for any home loan.

Our team at QuickHome Loan helps you balance these numbers. We guide you to find home loan structures that fit your cash flow without dry-docking your retirement dreams.

Key Points & Takeaways:

- EPF offers a high guaranteed rate of 8.25% with automatic employer contributions.

- PPF provides absolute tax-free safety up to 1.5 Lakh Rupees per financial year.

- NPS boosts long-term wealth through equity exposure and extra tax deductions.

- Limit your home loan EMI to 35% of take-home pay to protect your retirement savings.

Frequently Asked Questions (FAQ)

Q: Which has the highest interest rate among NPS, EPF, and PPF?

A: Currently, EPF offers a fixed interest rate of 8.25%, while PPF offers 7.10%. NPS is market-linked, meaning its equity and debt funds can deliver historical returns of 9% to 12% over the long term, though these are not guaranteed.

Q: Can I invest in both PPF and NPS at the same time?

A: Yes. You can invest in both schemes simultaneously. This strategy combines the guaranteed tax-free safety of PPF with the high inflation-beating growth potential of NPS.

Q: Are withdrawals from the National Pension System fully tax-free?

A: No. When you retire, you can withdraw up to 60% of your NPS corpus as a tax-free lump sum. You must use the remaining 40% to purchase an annuity, which provides a regular pension that is taxable based on your income slab.