Doctor Home Loan India 2026: Get 0.25% Lower Rate + 100% Processing Fee Waiver — Who Qualifies?

Get a Home Loan for Doctors in India with special 0.25% interest rate discounts and 100% processing fee waivers. Check your eligibility.

"Doctors in India can access custom home loans featuring low interest rates starting from 7.15 percent, an exclusive 0.25 percent rate discount, and a 100 percent processing fee waiver. Eligible applicants aged 21 to 65 with a 700 plus CIBIL score can apply using simple income proofs like 3 years of ITR and bank statements."

Home Loan for Doctors in India: Benefits, Eligibility and Apply Guide

Dr. Rohan spent twelve hours in the operating room only to face another headache at his office desk. He wanted to buy a home, but his bank manager did not understand why his private clinic had high revenues but fluctuating monthly cash flows. This is a common story. Securing a Home Loan for Doctors in India should be easy given your noble profession. Yet, many medical professionals face unexpected friction. Let us clear the confusion and show how you can secure your dream property with elite terms.

Why Doctors Get Special Treatment

Lenders view medical practitioners as premium borrowers. Your degrees command respect, and your earning power remains highly predictable over the long term. Whether you run a private clinic or work as a salaried surgeon at a corporate hospital, financial institutions trust your repayment capacity. Because your default rates remain exceptionally low, banks actively compete to win your business. They design custom loan products with high limits and flexible parameters just to have you on their books.

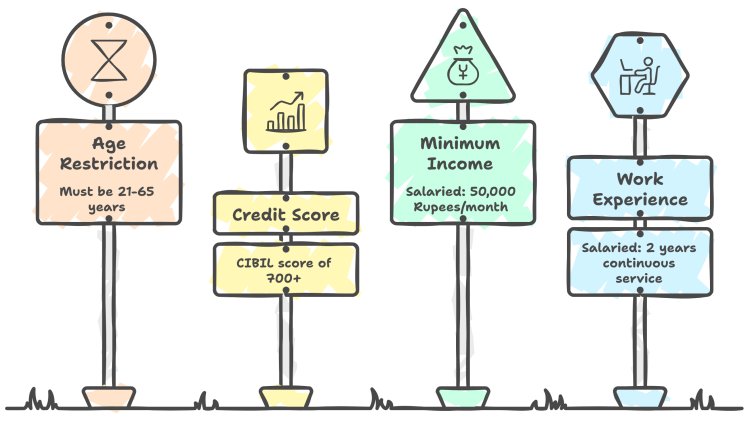

Eligibility Criteria for Medical Practitioners

Securing a doctor loan requires meeting standard parameters, but banks offer significant relaxations for medical professionals.

Here is the standard eligibility checklist:

- Age: You must be between 21 and 65 years old at the time of loan maturity.

- Credit Score: A CIBIL score of 700 or above secures the best interest rates.

- Minimum Income: Salaried doctors need a net monthly salary of at least 50,000 Rupees. Self-employed doctors must show annual business receipts above 5 Lakh Rupees.

- Work Experience: Salaried applicants need at least two years of continuous service. Private practitioners need a stable practice running for three years.

Relaxations for medical specialists often include lower minimum income thresholds and longer repayment terms up to 30 years. Banks also bypass standard business vintage checks if you hold a post-graduate medical degree.

Documents Required for a Fast Approvals

Keep your paperwork organized to speed up the approval process. You must submit documents from three distinct categories:

- Identity and Address Proof: Submit your PAN card, Aadhaar card, passport, or utility bills.

- Income Proof: Provide 3 Years ITR, Audited Profit and Loss Statement, and 6 Months Bank Statement. Salaried doctors must also submit three months of salary slips and Form 16.

- Property Documents: Include the registered sale agreement, approved building plan, and the previous title deeds of the property.

Key Benefits and Exclusive Perks

Doctors enjoy some of the most competitive financial terms in the country. Standard perks include high Loan-to-Value ratios up to 90 percent for properties below 30 Lakh Rupees and tax savings up to 2 Lakh Rupees on interest payments under Section 24b. You also get tax deductions up to 1.5 Lakh Rupees under Section 80C.

As a medical practitioner, you can access an exclusive perk: a 0.25 percent Interest Rate Discount and a 100 percent Processing Fee Waiver.

To check your personalized rates and claim these advantages, you can apply directly through the QuickHome Loan Doctor Portal at https://quickhomeloan.in/home-loan/profession/doctors

| Lender Name | Active Interest Rate |

|---|---|

| State Bank of India | 7.25% - 8.40% |

| HDFC Bank | 7.50% - 8.55% |

| ICICI Bank | 7.50% - 8.55% |

| Bank of Baroda | 7.15% - 8.35% |

| LIC Housing Finance | 7.25% onwards |

Common Challenges and How to Overcome Them

Private practice doctors often experience fluctuating practice revenues. Your monthly income might spike during some quarters and dip during others. Lenders sometimes struggle to compute an average monthly surplus from these uneven flows. If you recently took heavy loans to buy medical equipment, your debt-to-income ratio might look stretched.

To overcome this, present your audited financial statements clearly. Highlight your cash flow health rather than just your net taxable income. You can also pool your spouse's income to boost your borrowing capacity. If your spouse is a working professional, banks will gladly count their earnings to lower your debt ratio.

Key Points & Takeaways:

- Doctors are treated as low-risk borrowers by major lenders, resulting in customized loan options.

- Special perks include a 0.25 percent interest rate discount and a complete processing fee waiver.

- Income documentation requires a 3 Years ITR, Audited Profit and Loss Statement, and a 6 Months Bank Statement.

- Lenders benchmark home loans directly to the RBI repo rate, which is held steady at 5.25 percent.

Frequently Asked Questions (FAQ)

Q: What is the maximum home loan amount a doctor can get in India?

A: Lenders do not impose a fixed upper limit for medical professionals. Your maximum loan amount depends on your repayment capacity, annual income, and property value, often reaching up to 10 Crore Rupees or more.

Q: Can self-employed doctors get a home loan with fluctuating income?

A: Yes, self-employed doctors can secure home loans easily. Lenders evaluate your average earnings over three years using your audited profit and loss statements and tax returns to determine a stable borrowing limit.

Q: Are there any special interest rate discounts for doctors?

A: Yes, many premier Indian banks offer an exclusive 0.25 percent interest rate discount and a complete 100 percent processing fee waiver specifically to qualified medical professionals.

Q: Does a doctor need a co-applicant to apply for a home loan?

A: A co-applicant is not mandatory if your individual income meets the bank criteria. However, adding your spouse or a family member as a co-applicant can boost your eligible loan amount and tax benefits.

Q: What are the primary income documents required for a doctor home loan?

A: You must submit your 3 Years ITR, Audited Profit and Loss Statement, and 6 Months Bank Statement. Salaried doctors also need to provide three months of salary slips and Form 16.