What Is a CIBIL Score and Why It Matters for Your Home Loan

Learn what a CIBIL score is, how missed payments raise your home loan rates, and how to fix errors to secure the best rates under RBI repo guidelines.

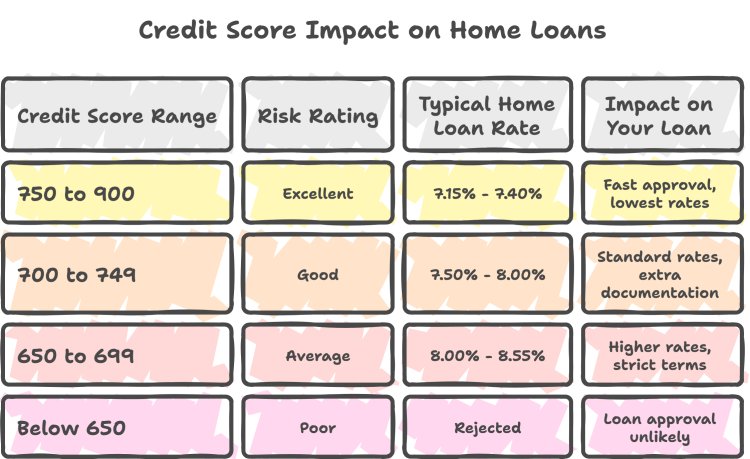

"A CIBIL score is a three-digit summary of your credit history, ranging from 300 to 900. It shows lenders how responsibly you manage debt. For a home loan, you need a score of 750 or higher to access the lowest interest rates and ensure fast approval."

What Is a CIBIL Score and Why It Matters for Your Home Loan

Amit assumed his clean bank balance of ten lakh rupees would guarantee an easy home loan. He was wrong. The bank rejected his application in minutes due to a forgotten credit card bill from his college days. A tiny mistake of two thousand rupees had wrecked his CIBIL score.

This scenario plays out across India every day. Your savings do not tell the whole story of your financial reliability. Your credit score does. Let us break down how this three-digit number dictates your home buying journey.

What Is a CIBIL Score?

Your CIBIL score is a three-digit number ranging from 300 to 900. It summarizes your credit history, borrowing behavior, and payment habits. TransUnion CIBIL, a credit information bureau licensed by the Reserve Bank of India, calculates this score.

Banks use this number to gauge how likely you are to pay back your debt. A higher score means you are a low-risk borrower. A lower score raises red flags immediately.

Why Your Score Dictates Your Interest Rate

Many home buyers do not realize that your CIBIL score determines the actual price of your loan. With the RBI repo rate holding steady at 5.25 percent, verified directly on rbi.org.in, banks peg their lending rates closely to this benchmark. However, they charge a risk premium based on your personal creditworthiness.

If you maintain a score of 750 or higher, you qualify for the best rates. If your score slips, your rate jumps.

Let us look at the math. On a home loan of fifty lakh rupees for twenty years, a rate of 7.15 percent from Bank of Baroda requires an EMI of about thirty-nine thousand rupees. If your score is low, HDFC or ICICI Bank might charge you 8.55 percent. That pushes your EMI to over forty-three thousand rupees. You end up paying nearly ten lakh rupees extra over the life of the loan. This is why a good score is not just a badge of honor, it is a massive money saver.

Silent Killers of Your Credit Rating

How does a score drop? It is rarely a single event. Here are the common culprits:

First, missed credit card payments. Even a single day of delay flags you in the system.

Second, high credit utilization. If you routinely use more than thirty percent of your credit card limit, bureaus assume you are starved for cash.

Third, settling a loan instead of paying it in full. A settled status on your report acts like a permanent red flag.

How to Dispute Errors on Your Report

Errors happen. A bank might forget to update your cleared loan status, or identity theft could create ghost accounts in your name. You must review your report at least twice a year to spot these slip-ups.

Here is how to fix them:

- Visit the official TransUnion CIBIL portal.

- Register your dispute online by selecting the specific incorrect entry.

- Submit proof of payment or closure documents.

The bureau must resolve the issue within thirty days under RBI rules.

QuickHome Loan helps you read between the lines of your credit report. We guide you through the process of repairing your credit profile before you apply for a major loan, ensuring you do not leave money on the table.

Key Points & Takeaways:

- A CIBIL score above 750 secures the lowest interest rates from Indian banks.

- Missed credit card payments or settling a loan instead of closing it severely damages your score.

- You can raise a free dispute on the TransUnion CIBIL portal to fix reporting errors within 30 days.

- A poor CIBIL score can cost you up to ten lakh rupees extra in interest charges over a 20-year loan term.

Frequently Asked Questions (FAQ)

Q: What is the minimum CIBIL score required for a home loan?

A: Most Indian banks require a minimum CIBIL score of 650 to consider a home loan, but you need a score of 750 or higher to get the lowest interest rates.

Q: How long does it take to update a CIBIL score?

A: Banks report your credit activity to TransUnion CIBIL every 30 to 45 days. Any changes or dispute resolutions will reflect on your score within this timeframe.

Q: Can I get a home loan with a bad CIBIL score?

A: Yes, but you will face higher interest rates, stricter terms, and must provide a co-applicant or guarantor with an excellent credit profile.