Home Insurance in India: What is Covered and What is Not

Learn exactly what Indian home insurance covers and excludes to protect your property and active bank loans in 2026

"Home insurance in India covers physical damage to your home structure caused by fire, natural disasters, and riots. It does not cover regular wear and tear, theft without forced entry, war, or damage to old construction. You can buy add-ons to cover personal belongings, jewellery, and temporary rent expenses."

Home insurance in India protects your biggest financial investment from unexpected disasters. Many home buyers believe that the property insurance packaged with their home loan covers everything. This is a costly mistake.

Let us break down what actually gets covered and where you are left exposed.

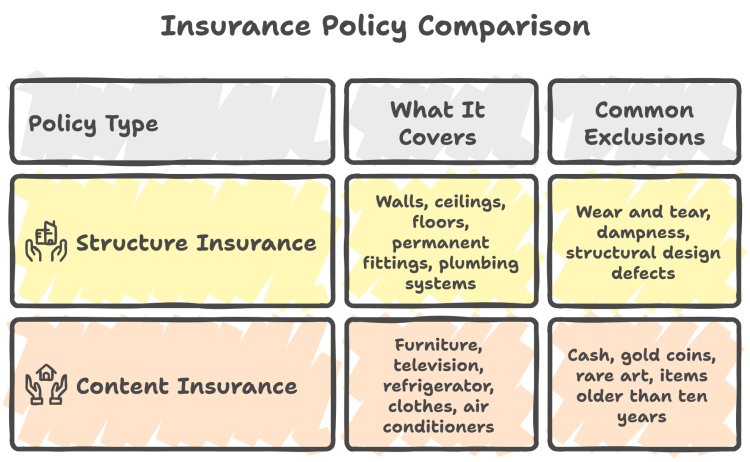

Structural Coverage versus Content Cover

Indian insurers divide policy protection into two distinct categories. Structure insurance covers the physical walls, roof, and permanent fixtures. Content insurance covers your indoor belongings like electronics, furniture, and appliances.

What is Covered under Standard Home Insurance?

Most standard policies in India operate on a multi-peril basis. This means they pay out for specific events.

Here is what is covered:

1. Natural Calamities: Damage caused by floods, earthquakes, landslides, storms, and cyclones.

2. Fire and Explosions: Accidental domestic fires, gas cylinder explosions, and lightning strikes.

3. Man-made Disruptions: Riots, strikes, and acts of malicious damage by third parties.

4. Burglary: Theft of items accompanied by actual forced entry into the premises.

What is Not Covered?

Understanding the gaps saves you from rejected claims later. Standard policies carry strict exclusions.

Here is what is not covered:

1. Depreciation: Normal wear and tear, rusting of pipes, and paint peeling due to age.

2. Wilful Negligence: Leaving the property vacant for more than thirty consecutive days without informing the insurer.

3. War and Nuclear Perils: Damage caused by war, invasions, or nuclear activity.

4. Cash and Documents: Loss of paper currency, stock certificates, or antique manuscripts.

Let us look at a real-life scenario. Ramesh bought a premium flat in Chennai. He secured a home loan at current competitive interest rates, choosing a top bank offering rates between 7.25 percent and 8.40 percent. When extreme floods hit Chennai, water damaged his ground-floor flat. Because Ramesh bought a comprehensive structural and content policy, the insurer paid 8 Lakh Rupees for wall repairs and damaged furniture. His neighbor, who only had the basic bank-mandated structure policy, received zero payout for ruined appliances.

How This Ties to Your Home Loan

When you apply for a mortgage, your lender wants to secure their asset. If you take an SBI home loan with active rates of 7.25 percent to 8.40 percent, or an ICICI Bank loan at 7.50 percent to 8.55 percent, the bank mandates property insurance.

This ensures that even if a major disaster strikes, the loan collateral remains protected. The benchmark repo rate stands at 5.25 percent as per the official Reserve Bank of India website at rbi.org.in. This anchor rate directly influences your borrowing cost. Protecting your home keeps your family secure while preventing personal financial ruin.

Action Steps to Take

First, read the fine print of your existing bank-provided policy. Second, estimate the actual replacement cost of your household contents. Third, purchase specific add-ons for expensive items like jewellery.

QuickHome Loan helps you understand these financial safety nets so you make smart, educated choices.

Key Points & Takeaways:

- Bank-mandated insurance usually covers only the building structure, not your household contents.

- Wear and tear, gradual depreciation, and self-inflicted damage are universally excluded from coverage.

- Add-ons are required to protect high-value personal assets like jewellery, cash, or art.

- A valid structural home policy protects you from paying EMIs on a destroyed property after major disasters.

Frequently Asked Questions (FAQ)

Q: Is home insurance mandatory for home loans in India?

A: Most Indian banks mandate structural home insurance to protect the mortgaged property against natural or man-made disasters before releasing the loan.

Q: Does standard home insurance cover theft?

A: Yes, but standard policies cover theft only under burglary, which requires evidence of violent or forced entry into your property.

Q: Are electronic items covered under home insurance?

A: Yes, electronic items are covered under the content insurance section of the policy, though you may need a separate add-on for high-value items.