You Need 20% Down Payment to Get a Home Loan: The Truth

Discover the truth about down payments for Indian home loans in 2026. Learn how much you really need for properties under 30 Lakh, 75 Lakh, and above

You Need 20% Down Payment to Get a Home Loan: The Truth

Are you sitting on the sidelines, waiting to save exactly 20% of your dream homes price before you even talk to a bank? You might be making a huge mistake. While you wait, property prices in cities like Bengaluru or Mumbai could climb faster than your savings account.

On the flip side, some buyers think they only need the down payment and forget about the hidden costs that the bank won’t cover. This confusion stops thousands of Indians from owning their own home every year

Quick Answer: In 2026, the amount you need to pay upfront depends on the price of the house. For a home under ₹30 Lakh, you only need 10%. If the home is between ₹30 Lakh and ₹75 Lakh, you need 20%. For homes above ₹75 Lakh, you need 25%.

Why do banks ask for a down payment at all?

Think of a home loan like a partnership. You and the bank are buying a house together. The bank wants to see that you have some skin in the game. If you put your own money into the house, you are less likely to stop paying your EMIs.

In finance, we call this the Loan-to-Value (LTV) ratio. It is just a fancy way of saying: What percentage of the houses price will the bank pay? If you pay 20% down, the LTV is 80%.

Is 20% the magic number for everyone?

Not at all. As of March 2026, the Reserve Bank of India (RBI) has very clear tiers based on the property’s value:

- Small Budget (Up to ₹30 Lakh): You only need to pay 10% from your pocket. The bank can give you a loan for the remaining 90%.

- Mid-Range (₹30 Lakh to ₹75 Lakh): This is where the 20% rule lives. The bank covers 80%.

- Luxury/Large Homes (Above ₹75 Lakh): You need to bring 25% to the table. The bank covers 75%.

Expert interjection: I often see buyers aiming for a 90% loan because they want to keep their cash. But remember, a higher loan means a higher interest rate. In 2026, banks typically charge 0.30% to 0.50% extra interest if you take a 90% loan compared to an 80% loan.

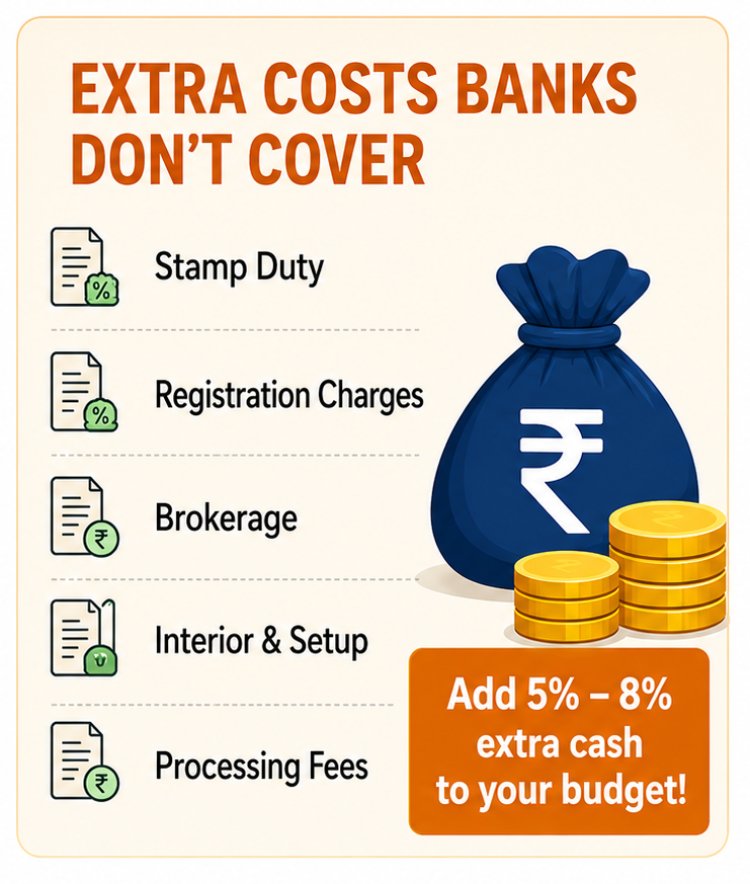

The Stamp Duty Trap: The cost no one talks about

Here is the real truth: The 20% down payment is not your total cost. Banks in India usually calculate the loan based only on the property’s agreement value. They do NOT include stamp duty, registration fees, or brokerage in the loan.

In 2026, stamp duty and registration can cost you between 5% and 8% of the property value depending on your state. If you are buying a ₹50 Lakh home, you need ₹10 Lakh for the 20% down payment PLUS roughly ₹3 Lakh to ₹4 Lakh for registration. If you only have ₹10 Lakh in the bank, you can’t buy that house yet.

Real-Life Scenario: Rahul’s Pune Apartment

My client Rahul wanted to buy a 2BHK in Pune for ₹60 Lakh. He had exactly ₹12 Lakh (20%) saved up. He thought he was ready.

When we sat down, I showed him the reality. Pune’s registration and stamp duty added another ₹4.2 Lakh to his cost. He also needed about ₹1 Lakh for basic woodwork and moving. He was actually ₹5 Lakh short.

Because we caught this early, he chose a slightly smaller ₹50 Lakh property instead. He stayed within his budget and didn’t have to take a high-interest personal loan to cover the gap.

Common Mistakes to Avoid

- Emptying your emergency fund: Never use your last rupee for a down payment. Keep 6 months of EMIs in a separate account for safety.

- Ignoring the Valuation Gap: If the banks valuer says the house is worth ₹45 Lakh but the seller wants ₹50 Lakh, the bank will only give you a loan based on ₹45 Lakh. You have to pay the ₹5 Lakh difference yourself.

- Forgetting the Processing Fees: Banks charge up to 0.5% as a fee to check your papers. It adds up.

Actionable Steps for You

- Check the Price Tier: Is your target home above or below ₹30 Lakh? This decides if you need 10% or 20%.

- Calculate the True Cost: Add 8% to the property price for taxes and fees.

- Get a Pre-Approval: Don’t guess. Ask a bank or a guide like QuickHome Loan exactly how much they will lend you based on your salary.

At QuickHome Loan, we believe a home loan should be a bridge to your dream, not a trap. We help you look past the marketing low EMI offers to see the real numbers. Use our educational resources to understand exactly how much cash you need before you sign that cheque.

Ready to see your real home-buying budget? Let’s find the transparency you deserve.

Frequently Asked Questions

Q.Can I get a 100% home loan in India in 2026?

No. RBI guidelines strictly prohibit banks from funding 100% of a property's value. You must contribute at least 10% to 25% as your 'own contribution' depending on the property price.

Q.Does the home loan cover stamp duty and registration?

Usually, no. Most Indian banks only finance the 'Agreement Value' or 'Market Value' of the property. You must pay for stamp duty, registration, and legal fees out of your own savings.

Q.Is it better to pay a higher down payment?

Yes, if you can afford it without touching your emergency funds. A higher down payment reduces your loan amount, which leads to lower monthly EMIs and often a lower interest rate from the bank.

Q.Can I use a personal loan for a home loan down payment?

While possible, it is highly risky. It increases your total monthly debt (FOIR), which might lead to the bank rejecting your home loan application altogether. It's better to save or use existing assets like PFs or gold.