How Much Term Insurance Do You Need for a Home Loan

Calculate the exact term insurance cover you need as a home loan borrower. Avoid expensive bank traps and protect your family with these rules

"As a home loan borrower, your term insurance cover must equal your total outstanding home loan balance plus ten times your annual income. This ensures your family can instantly pay off the bank and maintain their current standard of living if you are no longer there to pay the EMIs."

How Much Term Insurance Do You Need for a Home Loan

Many home buyers walk into a bank expecting to sign a home loan agreement, only to walk out with an expensive insurance policy they did not want. Banks often pressure you to buy a Home Loan Protection Plan, or HLPP, right alongside your loan. They might even tell you it is mandatory.

It is not.

Let us look at why buying a pure term insurance policy from the open market is almost always a smarter, cheaper decision for your household wealth.

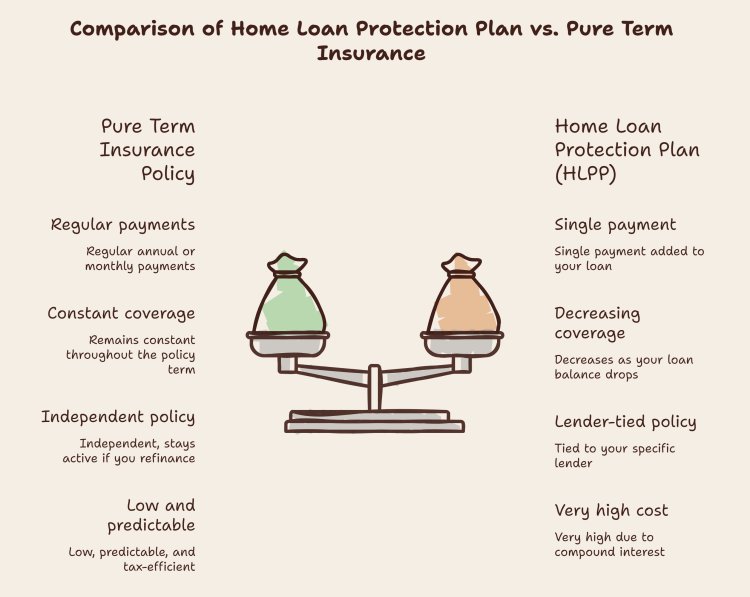

The Single Premium Trap and Why It Costs You More

Banks love selling HLPPs because they bundle the insurance premium directly into your home loan amount. If your home loan is ₹75 Lakh and the single insurance premium is ₹3 Lakh, the bank structures your loan as ₹78 Lakh.

You might think this is convenient. Here is the catch. You are now paying interest on that insurance premium for the next 15 or 20 years.

With current interest rates for major lenders like State Bank of India sitting between 7.25% and 8.40%, that extra ₹3 Lakh premium ends up costing you more than double in interest over the life of the loan.

Let us compare how a bank-sold loan protection plan stacks up against a pure term insurance policy.

The Golden Rule for Calculating Your Insurance Cover

How do you figure out the exact amount of cover you need? Do not just cover the loan balance. Your life is worth more than a bank debt.

Use this simple formula to find your ideal cover:

Total Term Cover Needed = Outstanding Loan Balance + (10 times your annual income) + personal liabilities - current liquid investments.

Let us use a realistic scenario to see how this works.

Meet Amit. He is a salaried professional earning ₹12 Lakh per year. He just secured a ₹75 Lakh home loan to buy an apartment in Pune. He also has active car loan debt of ₹5 Lakh and liquid mutual fund investments worth ₹10 Lakh.

Here is how Amit calculates his term insurance cover:

- Outstanding home loan: ₹75 Lakh

- Ten times annual income: ₹1.2 Crore (₹120 Lakh)

- Other liabilities: ₹5 Lakh

- Subtotal: ₹2 Crore

- Subtract liquid assets: Minus ₹10 Lakh

- Total cover needed: ₹1.9 Crore

If Amit only buys a basic loan protection plan for ₹75 Lakh, his family might clear the home loan if he passes away. However, they will have zero income replacement to pay for groceries, school fees, or medical bills. Buying a ₹2 Crore pure term policy protects his home and his family's daily survival.

Why Level Term Insurance Wins Over Reducing Cover

Banks sell reducing cover because the risk goes down as you pay off your principal. If your loan drops to ₹40 Lakh, your insurance cover drops to ₹40 Lakh.

Pure term insurance uses level cover. If you buy a ₹1 Crore policy, it remains ₹1 Crore on day one and day ten thousand.

This difference becomes vital if you decide to refinance your loan. If you transfer your home loan to another bank to chase a lower interest rate, your bank-linked HLPP usually lapses. A pure term policy stays with you no matter which bank holds your mortgage.

Having an independent policy gives you the freedom to switch lenders without losing your coverage.

Quick Steps to Secure Your Cover

First, check your existing term insurance policies to see if you already have enough cushion.

Second, tell your bank manager politely but firmly that you will source your own term insurance policy. You do not have to buy their bundled product.

Third, choose a term policy with a term that matches or exceeds your loan tenure.

We help home buyers navigate these choices at QuickHome Loan. We focus on clear financial education to help you protect your family without overpaying the banks. Talk to an expert today to evaluate your loan eligibility and protection options.

Key Points & Takeaways:

- Bank-sold Home Loan Protection Plans add the premium to your loan, forcing you to pay interest on your insurance cost.

- A pure term insurance policy is cheaper, keeps coverage constant, and remains active even if you transfer your loan to another lender.

- Calculate your coverage by adding your total loan balance to ten times your annual income.

- Lenders cannot legally force you to buy insurance directly from them to get a home loan approved.

Frequently Asked Questions (FAQ)

Q: Is it legally mandatory to buy insurance with a home loan in India?

A: No. The Reserve Bank of India (RBI) and the Insurance Regulatory and Development Authority of India (IRDAI) state that buying insurance from a lender is completely voluntary. Banks cannot legally reject your loan application solely because you refuse to buy their specific insurance policy.

Q: Can I use my existing term insurance policy to secure my home loan?

A: Yes. You can assign your existing pure term insurance policy to the bank by filling out an assignment form. However, make sure your existing cover is large enough to pay off the loan balance and still support your family's living costs.

Q: What happens to my home loan insurance if I prepay the loan early?

A: If you have a bank-linked single premium plan, you can apply for a partial refund of the premium for the remaining years. If you have a pure term insurance policy, you can simply choose to keep the policy active for your family's financial security or cancel it if you no longer need the cover.