"Minimum Salary for Home Loan in India 2026: ₹15,000? ₹25,000? ₹40,000? — See the Exact Table

Discover the minimum salary required for a home loan in India in 2026.

Minimum Salary for Home Loan

in India: Can You Qualify in 2026?

By CA Praphul Purohit

You found the perfect flat. You checked the amenities. Now you wonder if your pay check will satisfy the bank. As a former journalist, I have seen many buyers lose their dream home because they misunderstood one simple number: their net monthly income.

Let's get straight to the facts. For 2026, the Reserve Bank of India (RBI) maintains a focus on credit discipline. Banks do not just look at your gross salary. They look at what hits your bank account after taxes and PF.

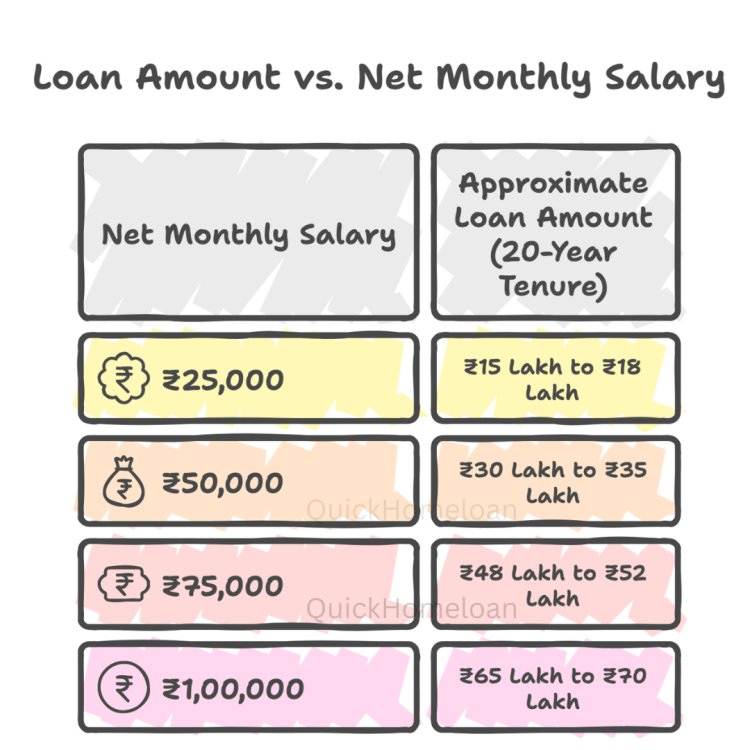

How much salary do you need for a home loan?

Most major lenders set the floor at ₹25,000 for applicants in Tier 1 cities like Mumbai, Delhi, or Bengaluru. If you live in a smaller town, some public sector banks might accept ₹15,000.

Here is the breakdown of salary versus the loan amount you can likely get:

Note: These figures assume a 9 percent interest rate. Rates vary based on your CIBIL score.

How do banks calculate your limit?

Banks use a formula called the Fixed Obligation to Income Ratio (FOIR). In simple terms, the bank wants to know how much money you have left after paying all your bills.

Most banks cap your total EMIs at 50 percent of your net pay. If you earn ₹60,000, the bank assumes you need ₹30,000 for food, rent, and life. That leaves only ₹30,000 for all your loans. If you already pay ₹10,000 for a car loan, the bank only has ₹20,000 left for your new home loan.

Next steps? Calculate your current debts before you apply.

Does your city change the rules?

Yes. The cost of living in a metro city is higher. Banks often increase the minimum salary floor for Mumbai or Gurgaon. They also look at your company category. Working for a Fortune 500 firm often helps you get a lower interest rate or a higher loan limit compared to a small startup.

Real Life Scenario: The Debt Trap

Meet Amit. He earns ₹80,000 a month in Bengaluru. He wanted a ₹50 Lakh loan. On paper, his salary is enough. However, Amit has a high-end bike loan and three active credit card EMIs. His total existing debt is ₹35,000.

Because his FOIR exceeded 50 percent, the bank rejected his application. Amit did not need a higher salary. He needed fewer debts. He cleared his credit card dues, and his application passed two months later.

How can you boost your eligibility?

If your salary is on the edge, do not worry. You have options.

- Add a Co-applicant: Adding a spouse or parent with an income combines both salaries. This is the fastest way to jump from a ₹30 Lakh limit to ₹60 Lakh.

- Choose a Longer Tenure: Spreading the loan over 25 or 30 years lowers the monthly EMI. This makes your current salary look more capable to the bank.

- Clear Small Debts: Close that old personal loan or gadget EMI before applying.

QuickHome Loan helps you navigate these numbers without the stress. We show you exactly where you stand before you talk to a lender.

Frequently Asked Questions

Q1. Can I get a home loan with a ₹15,000 salary?

Yes, some public sector banks and housing finance companies offer loans to individuals earning ₹15,000, especially in rural areas or for affordable housing schemes. However, the loan amount will be lower, likely around ₹8 to ₹10 Lakh.

Q2. Does my spouse's salary help in a home loan?

Adding your spouse as a co-applicant allows the bank to consider both incomes. This significantly increases your total loan eligibility.

Q3. Is gross salary or net salary used for calculation?

Banks primarily use your net monthly income (take-home pay) after deductions like Professional Tax, PF, and Income Tax to determine your EMI paying capacity.