Can Pensioners Get a Home Loan in India? Yes — If You Know These 5 Rules (2026)

Learn how to secure a home loan using pension income in 2026.

"Yes, you can apply for a home loan using pension income in 2026. Banks like SBI and LIC Housing Finance offer specialized schemes for retirees. You usually need a co-applicant (like a child or spouse) and must ensure the loan tenure ends before you turn 75."

How to Apply for a Home Loan Using Pension Income

You spent decades building a career. Now you want to build a home. Many retirees believe banks stop lending the moment the final salary cheque clears. That is a mistake. In May 2026, your pension is a powerful tool for property financing.

I have seen many retirees walk away from their dreams because a local branch manager looked at their age and frowned. Let us fix that. If you have a steady pension from the government or a reputable PSU, you have a solid income stream. The Reserve Bank of India (RBI) currently holds the repo rate at 5.25 percent. This stable rate makes May 2026 an ideal time to lock in a loan.

Directly from the official RBI website (rbi.org.in), we see this 5.25 percent benchmark allows banks to offer competitive rates even to senior citizens. Let us break down how you can use your pension to get that home.

Quick Answer: Pensioners can secure home loans by adding a younger co-applicant and opting for banks with dedicated senior citizen schemes. Interest rates currently start as low as 7.15 percent in May 2026.

Why do banks hesitate with pensioners?

Banks focus on two things: your ability to pay and your time to pay. When you are 65, the bank worries about the 20-year loan window. They see a shorter repayment period. They also worry that medical costs might eat into your pension income.

But here is the secret. Banks love stability. Your pension is more stable than many private-sector jobs today. To bridge the gap, you just need the right structure.

Can you meet the eligibility criteria?

Most Indian banks require you to be between 18 and 70 years old at the time of loan maturity. This means if you are 62 today, you might get a 10-to-12-year tenure.

Here is what you need to qualify: 1. A monthly pension from Central/State Government, Defence, or PSUs. 2. A credit score above 750. 3. A co-applicant, preferably a son or daughter with a steady income.

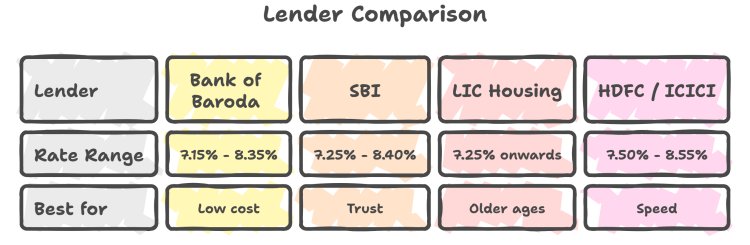

Current Interest Rates for May 2026

Banks are competing for reliable borrowers. Since the RBI repo rate is 5.25 percent, lenders have priced their products sharply.

A Real Life Example: Mr. Deshpande's Flat

Mr. Deshpande retired from the Railways with a monthly pension of 65,000 Rupees. He wanted to buy a 50 Lakh Rupee flat in Pune. At age 63, he feared rejection.

He applied with his daughter as a co-applicant. By adding her income of 80,000 Rupees, the bank saw a combined household income of 1.45 Lakh Rupees. They sanctioned a loan of 35 Lakh Rupees at 7.25 percent for a 12-year tenure. His EMI came to approximately 36,000 Rupees. Because his daughter was a co-owner, they also saved on stamp duty in Maharashtra.

Steps to secure your loan

First, check your pension bank. Most banks like SBI or PNB give better rates to people who already receive their pension in that specific branch.

Next, gather your documents. You need: 1. Your Pension Payment Order (PPO). 2. Form 16 or Income Tax Returns for the last 3 years. 3. Bank statements showing the last 6 pension credits. 4. Identity and property documents.

Lastly, keep your tenure short. Aim for 10 to 15 years. This reduces the risk for the bank and helps you stay debt-free sooner.

Key Points & Takeaways:

- Pension income is viewed as a stable income source by major Indian banks in 2026.

- The RBI repo rate of 5.25 percent keeps May 2026 interest rates between 7.15 percent and 8.55 percent.

- Adding a younger co-applicant is the most effective way to extend loan tenure.

- SBI and Bank of Baroda offer some of the most competitive rates for retirees.

- Loan maturity must typically occur before the applicant reaches age 75.

Next steps for your home journey

Do not let your retirement status stop you. The property market in May 2026 is favorable for buyers who have steady, documented income. Use your pension as your strength, not a limitation.

QuickHome Loan helps you navigate these specific bank requirements. We guide you through the paperwork so you can focus on picking the right floor for your new home.

Frequently Asked Questions (FAQ)

Q: What is the maximum age to apply for a home loan as a pensioner?

A: Most banks require the loan to be fully repaid by the time you turn 70 or 75. If you are 60, you can usually get a 10 to 15-year tenure.

Q: Is a co-applicant mandatory for pensioner home loans?

A: While not always mandatory, having a younger co-applicant with a steady income significantly increases your chances of approval and a longer tenure.

Q: Does the RBI repo rate affect my pension-based loan?

A: Yes. As of May 2026, the repo rate is 5.25 percent. Most home loans are linked to this rate (EBLR), so your interest rate will move in line with RBI decisions.

Q: Can I use my family pension to apply for a loan?

A: Yes, many banks accept family pension as a valid income source, though they may apply stricter loan-to-value (LTV) ratios.