10 First-Time Home Buyer Mistakes That Cost Lakhs in 2026

Learn the 10 common mistakes first-time home buyers make in 2026 that lead to losing lakhs.

"First-time buyers in 2026 often lose lakhs by ignoring credit scores, forgetting a 7-10 percent buffer for stamp duty and GST, and overstretching EMIs beyond 40 percent of income."

Buying your first home feels like a massive win. You have scouted the location and picked the floor plan. But as an investigative journalist who now looks at the math behind the bricks, I see buyers lose 10 to 20 Lakhs before they even move in. March 2026 brings new rules and rates that you must know.

Here is how to spot the traps.

Why do buyers pay more than they should?

Most people look at the property price and the EMI. They forget that the bank is selling a product, not a dream. If you do not check the fine print, you pay for the bank's profit instead of your own home. Let's break down the 10 blunders draining Indian bank accounts this year.

1. Ignoring the Credit Score Early On

In 2026, banks use the RBI external benchmark link strictly. If your score is below 750, you might pay 0.50 percent more interest. On a loan of 75 Lakhs for 20 years, that tiny gap costs you nearly 6 Lakhs extra. Check your score six months before you apply.

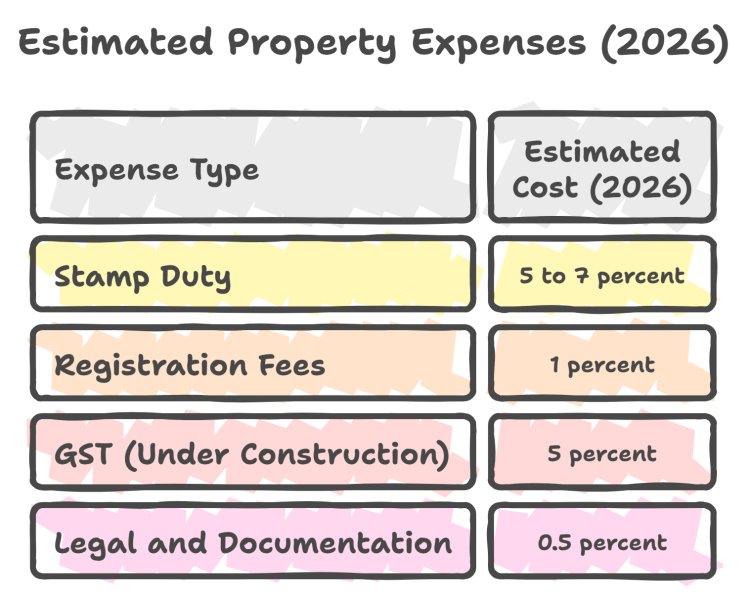

2. The Hidden Cost Shock

Many buyers forget that the price on the brochure is not the final price. You need to account for extras that can reach 12 percent of the property value.

3. Overstretching the EMI Ratio

I see many young couples commit 60 percent of their take-home pay to EMIs. This is a trap. If the RBI raises the repo rate by even 0.25 percent, your tenure or EMI will jump. Keep your total debt under 40 percent of your monthly income.

4. Falling for No EMI Till Possession

Developers offer these schemes to lure you in. Usually, the interest still builds up or the property price is inflated to cover the cost. You end up paying more interest over the long run. Always ask for the cash discount price instead.

5. Ignoring the Bank Spread

Banks do not just charge the repo rate. They add a spread. If the repo rate is 6.25 percent and your bank charges 8.75 percent, their spread is 2.50 percent. Negotiate this spread. A lower spread saves you lakhs over two decades.

6. Not Checking the RERA Carpet Area

Some builders still talk about super built-up area. This is old school and illegal. Always calculate the price based on the carpet area listed on the RERA website. If you pay for 1000 square feet but only get 700, you just lost 30 percent of your money.

7. Skipping Technical and Legal Checks

Do not trust the builder's legal report alone. Hire an independent lawyer to check the title deed and the occupancy certificate. Paying 15,000 Rupees now can save you from a 1 Crore loss later if the project hits a legal wall.

8. Forgetting Home Loan Insurance

Life is unpredictable. If something happens to the primary earner, the family loses the house. Banks push their own expensive policies. Shop around for a simple Term Insurance plan instead. It is often cheaper and offers better cover.

9. Underestimating Renovation and Maintenance

You buy the house for 1 Crore, but you need 15 Lakhs for interiors. Most people do not budget for this and take high-interest personal loans later. Add these costs to your initial plan.

10. Choosing the Wrong Tenure

A 30-year loan looks attractive because the EMI is low. However, you pay nearly double the principal in interest. Aim for a 15 or 20-year tenure and use yearly prepayments to kill the loan faster.

Key Takeaways

- Check your credit score 6 months before applying to avoid higher interest rates.

- Budget 10 to 12 percent extra for stamp duty, registration, and GST.

- Always use the RERA carpet area to calculate the true cost per square foot.

- Keep your total debt EMI under 40 percent of your monthly take-home pay.

- Compare the bank spread over the repo rate to save lakhs in interest.

Next Steps for You

- Download your credit report today.

- Save 15 percent of the property value for fees and interiors.

- Verify the project on the RERA portal.

- Use a home loan calculator to see the total interest cost.

At QuickHome Loan, we help you see through the marketing noise. We provide the tools to compare spreads and find the real cost of your dream home. Let's make sure your first home is an asset, not a debt trap.

Frequently Asked Questions

Q.What is a good credit score for a home loan in 2026?

A score of 750 or above is ideal. It helps you get the lowest interest rates and better negotiation power on the bank's spread.

Q.Does the RBI repo rate affect my existing home loan?

Yes, if you have a floating-rate loan linked to the external benchmark. When the RBI changes the repo rate, your bank usually adjusts your interest rate within three months.

Q.Is it better to take a longer tenure to keep EMIs low?

While a longer tenure lowers the monthly payment, it significantly increases the total interest you pay. It is better to choose the shortest tenure you can comfortably afford.

Q.Can I negotiate the processing fee with the bank?

Yes. Banks often waive or reduce processing fees during festive seasons or for applicants with high credit scores. Always ask for a waiver before signing.