Improve your CIBIL score from 600 to 750 with 7 steps

Clean up your credit report and raise your score from 600 to 750 with 7 proven steps. Secure low interest rates on home loans under RBI rules.

"To improve your CIBIL score from 600 to 750, check your credit report for errors on the official CIBIL site, lower your credit card utilization below 30 percent, and automate payments to avoid delays. Avoid applying for multiple loans simultaneously and pay your outstanding balances in full instead of settling them."

Improve your CIBIL score from 600 to 750 with 7 steps

Rohan thought his salary of ₹1.5 Lakh guaranteed a ₹50 Lakh home loan. He was wrong. His CIBIL score of 600 triggered immediate rejections. Many buyers believe income overrides credit history. It does not.

Your credit score acts as your financial passport. When you apply for a loan, banks look at this three-digit number first. With the Reserve Bank of India, official site rbi.org.in, holding the repo rate steady at 5.25%, lenders are selective. A score of 600 marks you as high risk. A score of 750 unlocks the lowest rates.

Here is how your score affects active interest rates:

| Bank Name | Rate for 750+ Score | Rate for 600 Score | Estimated Extra Cost on ₹50 Lakh Loan |

|---|---|---|---|

| State Bank of India | 7.25% | 8.40% | ₹35,000 extra per year |

| ICICI Bank | 7.50% | 8.55% | ₹37,500 extra per year |

| Bank of Baroda | 7.15% | 8.35% | ₹36,000 extra per year |

Let's break down the 7 steps to move your score to 750.

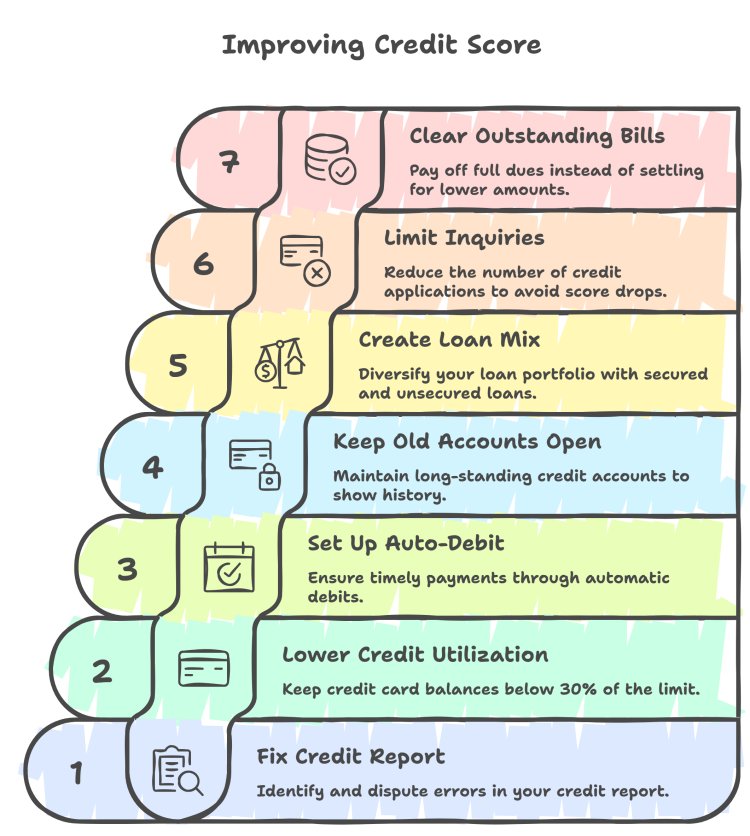

1. Fix mistakes in your credit report

Errors happen. A bank might report a paid loan as active. Pull your free CIBIL report. Look for wrong names, incorrect account numbers, or balance mismatches. Log a dispute on the official CIBIL website immediately if you spot errors.

2. Pay down credit card balances below 30 percent

If your card limit is ₹1 Lakh, do not spend more than ₹30,000. High spending tells banks you are credit-hungry. Pay off outstanding amounts to lower this ratio.

3. Set up auto-debit for your payments

Missing a payment hurts your score. Auto-pay your minimum dues. Even a brief delay of three days gets reported to bureaus, lowering your score.

4. Keep your oldest credit accounts open

The length of your credit history matters. Do not close old credit cards. They show banks you have handled credit responsibly for years.

5. Create a healthy mix of loans

Lenders like to see both secured loans like home loans and unsecured loans like credit cards. Having only personal loans hurts your risk profile.

6. Stop making multiple loan inquiries

Every time you apply for a credit card or loan, banks pull your report. This hard inquiry drops your score. Apply only when you must.

7. Clear outstanding bills instead of settling them

Avoid settling loans for a lower amount. A status of settled stays on your credit report for seven years, blocking future loans. Pay the full dues instead.

Next steps. Start by pulling your credit report today. At QuickHome Loan, we help you understand these numbers so you can buy your home with confidence.

Key Points & Takeaways:

- A CIBIL score of 750 helps you secure the lowest home loan interest rates starting at 7.15%.

- Identify and dispute reporting errors on the official CIBIL portal to boost your score quickly.

- Keep your credit utilization ratio below 30% to avoid appearing credit-hungry to lenders.

- Pay off outstanding loan balances completely instead of opting for a settlement.

Frequently Asked Questions (FAQ)

Q: How long does it take to improve a CIBIL score from 600 to 750?

A: It typically takes four to six months of consistent payment discipline, error correction, and low credit card utilization to see a significant jump in your CIBIL score.

Q: Can I get a home loan with a CIBIL score of 600?

A: It is difficult. Most top lenders like SBI and ICICI require a score of 700 or above. While some non-banking financial companies (NBFCs) might approve it, they will charge much higher interest rates.

Q: Does checking my own CIBIL score lower it?

A: No. Checking your own credit score is a soft inquiry. It does not impact your score. Only hard inquiries initiated by lenders when you apply for loans lower your score.