Home Loan Documents Required in India 2026: Complete Checklist (Salaried + Self-Employed)

Stop chasing banks. Use this clear checklist for your 2026 home loan application.

"To get your home loan approved in 2026, you need three sets of papers. First, KYC documents like your Aadhaar and PAN. Second, income proof such as 3 months of salary slips or 2 years of ITR. Third, property documents including the sale agreement and allotment letter."

Most buyers lose their dream home because of one missing paper. It sounds small. It feels minor. But a single missing signature or an old bank statement can stall your ₹75 Lakh loan for weeks. You do not want that stress when the builder asks for payment.

As of May 19, 2026, the RBI keeps a tight watch on lending. Banks are faster now, but they are also pickier. If your file is messy, they move to the next person. Let us fix your file today.

To secure a home loan in 2026, gather your KYC (Aadhaar, PAN), income proof (Salary slips, ITR, Form 16), and property papers (Sale deed, Tax receipts). Having these ready can reduce your approval time from fifteen days to just forty-eight hours

Why do banks reject your paperwork?

Banks do not hate your application. They hate risk. If your documents do not tell a clear story about your money, the bank says no. Often, people submit blurred copies or outdated bank statements. These tiny errors scream high risk to a credit officer.

Your Identity Check (KYC)

This is the easiest part. You must prove who you are and where you live. Since the 2025 digital update, most banks fetch this via e-KYC. Still, keep physical copies ready.

- PAN Card. This is your financial fingerprint.

- Aadhaar Card. Ensure your mobile number matches your Aadhaar.

- Passport sized photos. Use recent ones from this year.

- Proof of residence. A utility bill or rent agreement works if your Aadhaar has an old address.

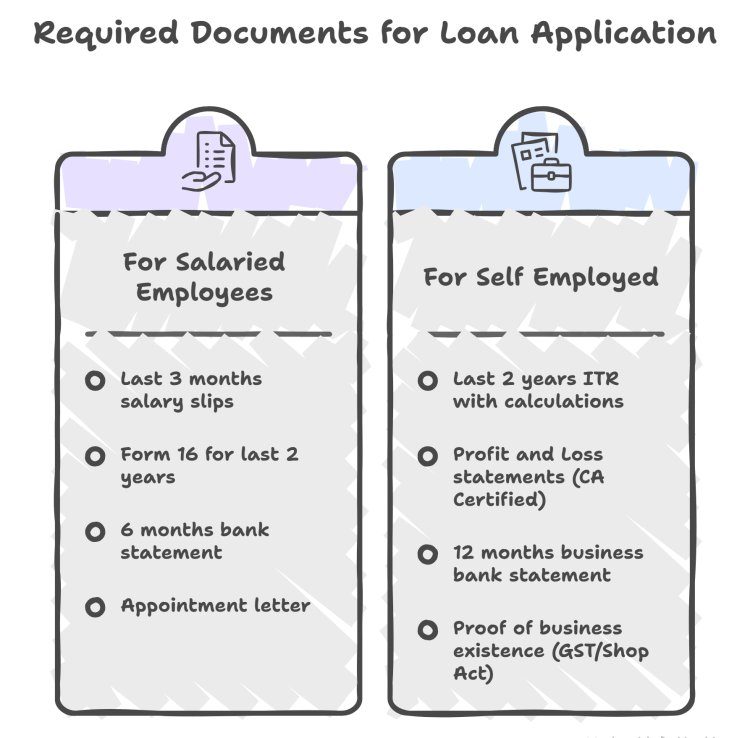

Proving Your Income

Banks want to see that you can pay them back. Think of it like a rental agreement. The bank is renting you money. They need to see your earnings are steady.

The Property File

The bank needs to know the house is legal. They will send a lawyer to check these. If you are buying from a builder, ask for the legal set.

- Copy of the Sale Agreement. This must be registered.

- Allotment Letter. This proves the flat is yours.

- Possession Letter. Only if the building is ready

- No Objection Certificate (NOC). Usually from the society or builder.

- Property Tax receipts. These prove the seller has paid their dues.

A Real Life Mess

Last month, a client named Amit found a flat in Pune for ₹90 Lakh. He had a great salary of ₹1.5 Lakh per month. He thought the loan was a sure thing. But Amit forgot his Form 16 from his previous employer. The bank stopped the process. By the time he got the paper, another buyer with a ready file took the flat. Amit lost the home because of one folder. Do not be like Amit. Gather your papers before you visit a site.

Key Takeaways

- KYC, Income, and Property papers form the tripod of a successful loan application.

- Digital copies are necessary, but original documents are required for final verification.

- Self-employed individuals need at least two years of audited business records.

- A clean document file can speed up your loan sanction by several days.

Your Action Checklist

- Scan everything into a single PDF folder on your phone.

- Update your Aadhaar address if you moved recently.

- Download your latest 6 month bank statement in PDF format.

- Check if your PAN is linked to your Aadhaar.

QuickHome Loan helps you organize this file before you even talk to a bank. We act as your guide to ensure no paper is missing. This preparation makes you a preferred borrower. You get better rates and faster calls

Frequently Asked Questions

Q.Can I get a home loan without a PAN card in 2026?

No. A PAN card is mandatory for all home loan applications in India as it tracks your credit history and tax compliance.

Q.What if I do not have a Form 16?

If you do not have Form 16, you can provide your ITR filings for the last two years along with a salary certificate from your HR department.

Q.How old can my bank statements be?

Banks require your most recent 6 months of statements. If you apply in March 2026, your statements should cover September 2025 to February 2026.