GST on under-construction property: everything buyers must know in 2026

Learn how GST on under-construction property affects your budget. Calculate tax rates and EMIs with standard market rates

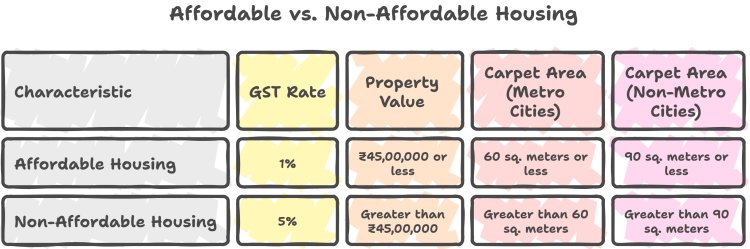

"GST on under-construction property charges a 1% tax for affordable homes valued under ₹45,00,000 and a 5% tax for other residential properties. Ready-to-move homes with a completion certificate attract 0% tax. This levy directly increases your total acquisition cost and your monthly loan outlay."

Tax Rules Redefining Your Dream Home Budget

Buying a home brings immense joy, but hidden taxes can quieten your celebrations. If you choose an unfinished flat, you must pay Goods and Services Tax, commonly known as GST (Goods and Services Tax). This direct levy alters your final purchase cost. To make a smart choice, you must know how the GST On Under Construction tax structure affects your pocket. Let's break it down. When you buy a flat before its completion, the government views it as a service supplied by the builder, which attracts this tax. Ready-to-move-in properties with a completion certificate do not attract this levy. This distinction changes your financial planning.

Decoupling the Goods and Services Tax Math for Property Buyers

The tax structure separates properties into affordable and non-affordable segments. Affordable housing attracts a lower tax rate of 1% without Input Tax Credit, which we call ITC (Input Tax Credit). To qualify as affordable, the property value must stay under ₹45,00,000, and the carpet area must not exceed 60 square meters in metro cities. Non-affordable housing attracts a 5% tax rate without ITC. What is ITC? Think of ITC as a discount coupon. Builders used to get tax refunds on materials like cement and steel, which they passed to you. Now, builders pay flat rates without claiming these refunds back. The government applies GST On Under Construction houses differently compared to ready-to-move-in flats to balance the tax collection. Here is why this matters. Since builders cannot claim tax refunds on raw materials, they often add these costs directly to the base price of your home.

Calculating Your Actual Outgo and Home Loan Math

Your total outgo includes the base price plus the GST On Under Construction rate. Let's look at how this tax combines with your home loan. If you take a loan at the current standard market reference rate of 7.10% p.a. from the State Bank of India, which we call SBI (State Bank of India), your monthly outlay rises. The Reserve Bank of India, known as RBI (Reserve Bank of India), maintains the repo rate at 5.25%. This rate acts as the baseline for your bank. We can compare an Equated Monthly Installment, known as EMI (Equated Monthly Installment), to sharing a massive sandcastle into equal smaller daily cups so it is easier to assemble over time. Let us evaluate two distinct scenarios using standard market rates to see the real math.

|

Property Value |

GST Rate Applied |

Added Tax Outflow |

Loan Amount at 7.10% |

Estimated Monthly EMI |

|

₹40,00,000 |

1% |

₹40,000 |

₹32,00,000 |

₹25,007 |

|

₹50,00,000 |

5% |

₹2,50,000 |

₹40,00,000 |

₹31,259 |

|

₹1,00,00,000 |

5% |

₹5,00,000 |

₹80,00,000 |

₹62,518 |

As shown, the tax adds ₹2,50,000 to a ₹50,00,000 home, and ₹5,00,000 to a ₹1,00,00,000 home. This extra cost increases your required down payment or expands your loan size, raising your monthly EMI.

Watchpoints for Smart Property Investors

Before you sign any papers, keep these three points in mind:

- Completion Certificate: Ensure you check if the developer has received the official completion certificate. If they have, you pay 0% tax.

- Land Value Deduction: Developers get a one-third deduction for land value from the total contract value. The tax applies only to the remaining two-thirds of the property cost.

- Cooperative Society Charges: Maintenance charges or electricity deposits might attract separate tax rates. Always ask for a clear breakup from your developer.

Your Action Plan for Smarter Property Purchases

Buying a home is a major step. You must plan your cash flows carefully. Calculating the exact GST On Under Construction liability before signing the builder-buyer agreement prevents unexpected financial shocks. Talk to your developer and get a written estimate of all tax charges. Next steps. Use online calculators to see how these taxes alter your monthly loan outgo. If you need help calculating your home loan EMI or comparing different bank rates, QuickHome Loan provides simple guides and calculators to assist your path. They help you make clear, stress-free decisions.

Key Takeaways Checklist

- Affordable homes under ₹45,00,000 attract a low 1% GST rate.

- Non-affordable properties attract a 5% GST rate without tax credit benefits.

- Ready homes with a completion certificate enjoy a 0% GST rate.

Frequently Asked Questions

Q: Does GST apply to ready-to-move-in flats?

No. If a developer has received the completion certificate, the property attracts 0% GST.

Q: What is the GST rate for affordable homes?

Affordable homes under ₹45,00,000 attract a 1% GST rate.

Q: How does GST affect my home loan amount?

Since GST increases the total property cost, your required loan size and monthly EMI increase proportionately.